Feature Selection Based on Univariate ROC_AUC for Classification and MSE for Regression | Machine Learning | KGP talkie

Feature Selection Based on Univariate ROC_AUC for Classification and MSE for Regression

Watch Full Playlist: https://www.youtube.com/playlist?list=PLc2rvfiptPSQYzmDIFuq2PqN2n28ZjxDH

What is ROC_AUC

The Receiver Operator Characteristic (ROC) curve is well-known in evaluating classification performance. Owing to its superiority in dealing with imbalanced and cost-sensitive data, the ROC curve has been exploited as a popular metric to evaluate ML models.

The ROC curve and AUC (area under the ROC curve) have been widely used to determine the classification accuracy in supervised learning.

It is basically used in Binary Classification

Use of ROC_AUC in Classification Problem

Importing required libraries

import numpy as np import pandas as pd import matplotlib.pyplot as plt import seaborn as sns

from sklearn.model_selection import train_test_split from sklearn.ensemble import RandomForestClassifier from sklearn.metrics import accuracy_score, roc_auc_score from sklearn.feature_selection import VarianceThreshold

Download Dataset: https://github.com/laxmimerit/Data-Files-for-Feature-Selection

Let’s read the santander data inti the data variable.

data = pd.read_csv('train.csv', nrows = 20000)

data.head()

| ID | var3 | var15 | imp_ent_var16_ult1 | imp_op_var39_comer_ult1 | imp_op_var39_comer_ult3 | imp_op_var40_comer_ult1 | imp_op_var40_comer_ult3 | imp_op_var40_efect_ult1 | imp_op_var40_efect_ult3 | … | saldo_medio_var33_hace2 | saldo_medio_var33_hace3 | saldo_medio_var33_ult1 | saldo_medio_var33_ult3 | saldo_medio_var44_hace2 | saldo_medio_var44_hace3 | saldo_medio_var44_ult1 | saldo_medio_var44_ult3 | var38 | TARGET | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 1 | 2 | 23 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0 | 0 | … | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 39205.170000 | 0 |

| 1 | 3 | 2 | 34 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0 | 0 | … | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 49278.030000 | 0 |

| 2 | 4 | 2 | 23 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0 | 0 | … | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 67333.770000 | 0 |

| 3 | 8 | 2 | 37 | 0.0 | 195.0 | 195.0 | 0.0 | 0.0 | 0 | 0 | … | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 64007.970000 | 0 |

| 4 | 10 | 2 | 39 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0 | 0 | … | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 117310.979016 | 0 |

5 rows × 371 columns

Here, we will remove the target.

X = data.drop('TARGET', axis = 1)

y = data['TARGET']

X.shape, y.shape

((20000, 370), (20000,))

Let’s split this dataset into train and test datasets using the below code.

Here test_size = 0.2 that means 20% for testing and remaining for training the model.

X_train, X_test, y_train, y_test = train_test_split(X, y, test_size = 0.2, random_state = 0, stratify = y)

Remove Constant, Quasi Constant and Duplicate Features

In this, first we need to create a variance threshold and then fit the model with training set of the data.

#remove constant and quasi constant features constant_filter = VarianceThreshold(threshold=0.01) constant_filter.fit(X_train) X_train_filter = constant_filter.transform(X_train) X_test_filter = constant_filter.transform(X_test) X_train_filter.shape, X_test_filter.shape

((16000, 245), (4000, 245))

370-245

125

If two features are exactly same those are called as duplicate features that means these features doesn’t provide any new information and makes our model complex.

Here we have a problem as we did in quasi constant and constant removal sklearn doesn’t have direct library to handle with duplicate features .

So, first we will do transpose the dataset and then python have a method to remove duplicate features.

Let’s transpose the training and testing dataset by using following code.

#remove duplicate features X_train_T = X_train_filter.T X_test_T = X_test_filter.T X_train_T = pd.DataFrame(X_train_T) X_test_T = pd.DataFrame(X_test_T)

Let’s get the total number of duplicated features .

X_train_T.duplicated().sum()

18

duplicated_features = X_train_T.duplicated()

features_to_keep = [not index for index in duplicated_features] X_train_unique = X_train_T[features_to_keep].T X_test_unique = X_test_T[features_to_keep].T X_train_unique.shape, X_train.shape

((16000, 227), (16000, 370))

Now calculate ROC_AUC Score

NOw, we will calculate roc_auc score for each feature. Let’s have a look at the following code.

roc_auc = []

for feature in X_train_unique.columns:

clf = RandomForestClassifier(n_estimators=100, random_state=0)

clf.fit(X_train_unique[feature].to_frame(), y_train)

y_pred = clf.predict(X_test_unique[feature].to_frame())

roc_auc.append(roc_auc_score(y_test, y_pred))

print(roc_auc)

[0.5020561820568537, 0.5, 0.5, 0.49986968986187125, 0.501373452866903, 0.49569976544175137, 0.5028068643863192, 0.49986968986187125, 0.5, 0.5, 0.4997393797237425, 0.5017643832812891, 0.49569976544175137, 0.49960906958561374, 0.49895751889497003, 0.49700286682303885, 0.49960906958561374, 0.5021553136956755, 0.4968725566849101, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.49986968986187125, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5029371745244479, 0.4959603857180089, 0.5, 0.5048318679438659, 0.4997393797237425, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.49921813917122754, 0.49921813917122754, 0.49824600955181303, 0.5, 0.5, 0.5, 0.4990878290330988, 0.4983763196899418, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5025462441100617, 0.4990878290330988, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.49986968986187125, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.4997393797237425, 0.5, 0.5, 0.49986968986187125, 0.4991581805187143, 0.4988272087568413, 0.49674224654678134, 0.4995491109331005, 0.5, 0.5, 0.5022856238338043, 0.5012431427287742, 0.5, 0.5, 0.5, 0.49986968986187125, 0.5, 0.4997393797237425, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5, 0.5076595179963898]

Let’s put these values in the pandas series and sort them into descending order.

roc_values = pd.Series(roc_auc) roc_values.index = X_train_unique.columns roc_values.sort_values(ascending =False, inplace = True)

roc_values

244 0.507660

107 0.504832

104 0.502937

6 0.502807

155 0.502546

...

18 0.496873

211 0.496742

105 0.495960

12 0.495700

5 0.495700

Length: 227, dtype: float64The features which are less than or equals to 0.5 won’t provide any information for the classification.

roc_values.plot.bar()

plt.title('roc_auc score with respect to the features')

plt.show()

Let’s go ahead and delet the features which have roc_auc score less than 0.5.

sel = roc_values[roc_values>0.5] sel

244 0.507660 107 0.504832 104 0.502937 6 0.502807 155 0.502546 215 0.502286 17 0.502155 0 0.502056 11 0.501764 4 0.501373 216 0.501243 dtype: float64

Let’s selct new training and testing datasets by using `roc_auc score’.

X_train_roc = X_train_unique[sel.index] X_test_roc = X_test_unique[sel.index]

Build the Model and compare the performance

We will define a random forest classifier with 100 number of estimators.

def run_randomForest(X_train, X_test, y_train, y_test):

clf = RandomForestClassifier(n_estimators=100, random_state=0, n_jobs=-1)

clf.fit(X_train, y_train)

y_pred = clf.predict(X_test)

print('Accuracy on test set: ', accuracy_score(y_test, y_pred))

Let’s calculate the accuaracy and training time on test dataset.

%%time run_randomForest(X_train_roc, X_test_roc, y_train, y_test)

Accuracy on test set: 0.95275 Wall time: 917 ms

X_train_roc.shape

(16000, 11)

Let’s calculate the accuaracy and training time on original test dataset

%%time run_randomForest(X_train, X_test, y_train, y_test)

Accuracy on test set: 0.9585 Wall time: 1.76 s

Feature Selection using RMSE in Regression

from sklearn.datasets import load_boston from sklearn.linear_model import LinearRegression

from sklearn.metrics import mean_absolute_error, mean_squared_error, r2_score

boston = load_boston() print(boston.DESCR)

.. _boston_dataset:

Boston house prices dataset

---------------------------

**Data Set Characteristics:**

:Number of Instances: 506

:Number of Attributes: 13 numeric/categorical predictive. Median Value (attribute 14) is usually the target.

:Attribute Information (in order):

- CRIM per capita crime rate by town

- ZN proportion of residential land zoned for lots over 25,000 sq.ft.

- INDUS proportion of non-retail business acres per town

- CHAS Charles River dummy variable (= 1 if tract bounds river; 0 otherwise)

- NOX nitric oxides concentration (parts per 10 million)

- RM average number of rooms per dwelling

- AGE proportion of owner-occupied units built prior to 1940

- DIS weighted distances to five Boston employment centres

- RAD index of accessibility to radial highways

- TAX full-value property-tax rate per $10,000

- PTRATIO pupil-teacher ratio by town

- B 1000(Bk - 0.63)^2 where Bk is the proportion of blacks by town

- LSTAT % lower status of the population

- MEDV Median value of owner-occupied homes in $1000's

:Missing Attribute Values: None

:Creator: Harrison, D. and Rubinfeld, D.L.

This is a copy of UCI ML housing dataset.

https://archive.ics.uci.edu/ml/machine-learning-databases/housing/

This dataset was taken from the StatLib library which is maintained at Carnegie Mellon University.

The Boston house-price data of Harrison, D. and Rubinfeld, D.L. 'Hedonic

prices and the demand for clean air', J. Environ. Economics & Management,

vol.5, 81-102, 1978. Used in Belsley, Kuh & Welsch, 'Regression diagnostics

...', Wiley, 1980. N.B. Various transformations are used in the table on

pages 244-261 of the latter.

The Boston house-price data has been used in many machine learning papers that address regression

problems.

.. topic:: References

- Belsley, Kuh & Welsch, 'Regression diagnostics: Identifying Influential Data and Sources of Collinearity', Wiley, 1980. 244-261.

- Quinlan,R. (1993). Combining Instance-Based and Model-Based Learning. In Proceedings on the Tenth International Conference of Machine Learning, 236-243, University of Massachusetts, Amherst. Morgan Kaufmann.

X = pd.DataFrame(boston.data, columns=boston.feature_names) X.head()

| CRIM | ZN | INDUS | CHAS | NOX | RM | AGE | DIS | RAD | TAX | PTRATIO | B | LSTAT | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 0.00632 | 18.0 | 2.31 | 0.0 | 0.538 | 6.575 | 65.2 | 4.0900 | 1.0 | 296.0 | 15.3 | 396.90 | 4.98 |

| 1 | 0.02731 | 0.0 | 7.07 | 0.0 | 0.469 | 6.421 | 78.9 | 4.9671 | 2.0 | 242.0 | 17.8 | 396.90 | 9.14 |

| 2 | 0.02729 | 0.0 | 7.07 | 0.0 | 0.469 | 7.185 | 61.1 | 4.9671 | 2.0 | 242.0 | 17.8 | 392.83 | 4.03 |

| 3 | 0.03237 | 0.0 | 2.18 | 0.0 | 0.458 | 6.998 | 45.8 | 6.0622 | 3.0 | 222.0 | 18.7 | 394.63 | 2.94 |

| 4 | 0.06905 | 0.0 | 2.18 | 0.0 | 0.458 | 7.147 | 54.2 | 6.0622 | 3.0 | 222.0 | 18.7 | 396.90 | 5.33 |

y = boston.target

X_train, X_test, y_train, y_test = train_test_split(X, y, test_size = 0.2, random_state = 0)

Let’s calculate the mean square error(mse) between testing and predicting values of y

mse = []

for feature in X_train.columns:

clf = LinearRegression()

clf.fit(X_train[feature].to_frame(), y_train)

y_pred = clf.predict(X_test[feature].to_frame())

mse.append(mean_squared_error(y_test, y_pred))

mse

[76.38674157646072, 84.66034377707905, 77.02905244667242, 79.36120219345942, 76.95375968209433, 46.907351627395315, 80.3915476111525, 82.61874125667718, 82.46499985731933, 78.30831374720843, 81.79497121208001, 77.75285601192718, 46.33630536002592]

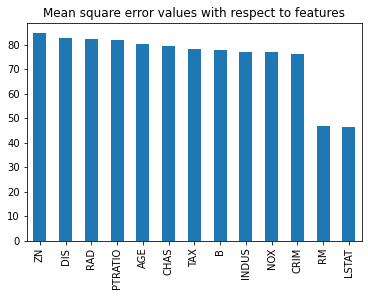

Let’s sort the mean square error values in descending order. Let’s have a look at the following code.

mse = pd.Series(mse, index = X_train.columns) mse.sort_values(ascending=False, inplace = True) mse

ZN 84.660344 DIS 82.618741 RAD 82.465000 PTRATIO 81.794971 AGE 80.391548 CHAS 79.361202 TAX 78.308314 B 77.752856 INDUS 77.029052 NOX 76.953760 CRIM 76.386742 RM 46.907352 LSTAT 46.336305 dtype: float64

Let’s observe the mean square error values with respect to features from the following bar plot.

mse.plot.bar()

plt.title('Mean square error values with respect to features')

plt.show()

Let’s create testing and training datasets based on only two features.

X_train_2 = X_train[['RM', 'LSTAT']] X_test_2 = X_test[['RM', 'LSTAT']]

Now, we will calculate the performance with the selected features.

%%time

model = LinearRegression()

model.fit(X_train_2, y_train)

y_pred = model.predict(X_test_2)

print('r2_score: ', r2_score(y_test, y_pred))

print('rmse: ', np.sqrt(mean_squared_error(y_test, y_pred)))

print('sd of house price: ', np.std(y))

r2_score: 0.5409084827186417 rmse: 6.114172522817782 sd of house price: 9.188011545278203 Wall time: 3 ms

Now, we will calculate the performance with the original features.

%%time

model = LinearRegression()

model.fit(X_train, y_train)

y_pred = model.predict(X_test)

print('r2_score: ', r2_score(y_test, y_pred))

print('rmse: ', np.sqrt(mean_squared_error(y_test, y_pred)))

print('sd of house price: ', np.std(y))

r2_score: 0.5892223849182507 rmse: 5.783509315085135 sd of house price: 9.188011545278203 Wall time: 4 ms

0 Comments